Today Ed Miliband formally launched the Labour Election Manifesto 2015. See the summary at the BBC.

David Cameron has called it a con trick. (Hattip Conservative Home)

This con trick claim can be substantiated by reading the Manifesto. Here are a few snippets.

The Economy

On the Economy, Labour realize they have an uphill struggle. A couple of examples

“We will cut the deficit every year with a surplus on the current budget..”

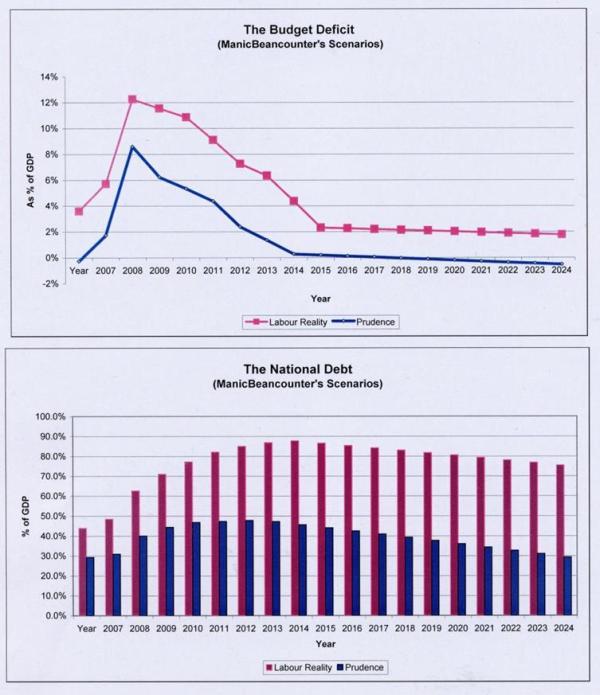

The current budget deficit is the difference between tax revenue and current spending. To get the total deficit you need to add in (what used to be called) capital expenditure.

Remember Gordon Brown’s Golden Rule of only borrowing to invest?

Ed Miliband will return Britain to the days of 2001-2008, when Labour built a structural deficit of £50-£70bn. It is this reason that there is still a huge deficit, not the credit crunch. Labour still do not understand the public sector capital investment does not provide financial returns. New roads, schools and hospitals are not constructed to generate revenue like in a business but to provide social returns. Properly spent, overall welfare is increased, despite capital spending creating additional financial burdens in terms of staffing and maintenance.

“There is not a single policy in this manifesto that is funded by additional borrowing.”

This is grossly misleading. Labour are committed to at least maintaining current spending levels. When there is a deficit that means new additional borrowing is required, adding to the total debt. What Labour mean is that additional spending will be funded by additional taxes.

Discouraging entrepreneurship, jobs and growth

There is a subsection headed “We will back our entrepreneurs and businesses”

The measures are tiny. Instead here are a scattering of policy initiatives which will likely damage British businesses and help undermine economic growth.

-

“We will reverse the Government’s top-rate tax cut.“

British Entrepreneurs will be discouraged from investing in Britain. They will go elsewhere.

-

“We will abolish the non-dom rules…”

Ed Balls in January said

“I think if you abolish the whole (nom-dom) status then probably it ends up costing Britain money”

There on a lot of people who rely on the non-doms for jobs. Many invest money in Britain.

-

“We will close tax loopholes that cost the public billions of pounds a year,”

The tax system will become even more complex, especially for small businesses. This could reduce revenues.

-

“We will end unfair tax breaks used by hedge funds and others“

A major part of Britain’s exports come from the financial services sector. Labour’s antipathy to this sector threatens hundreds of thousands of jobs and may demote the City of London to a second tier financial sector.

-

“We will increase the National Minimum Wage

We will ban exploitative zero-hours contracts

We will promote the Living Wage”

The cost of employing people will rise. Businesses who do not toe the official line on the living wage might be unable to sell to the State Sector. Start-up businesses will be reduced and small businesses will not expand as inflexible employment laws will increase the risks of taking people on. The unemployed will become locked out of jobs. Youth unemployment will rise.

-

“We will freeze gas and electricity prices until 2017“

Prices have been rising because of the Climate Change Act 2008 that Ed Miliband was responsible for steering through Parliament. There is huge investment needed in new sources of electricity. That ain’t going to happen if profit rates fall. This is a policy to ensure the lights go out in a couple of winters time.

-

“We will introduce a fairer deal for renters“

This will be at the expense of landlords, many of whom rent as a business.

-

“We will expand free childcare from 15 to 25 hours per week for parents of three- and four-year-olds, paid for with an increase in the bank levy.”

See point 4 on the City of London

I am really concerned that a Labour Government will jeopardize the prosperity of this country, and my children’s future. Rather than learning from past Labour continue to deceive themselves through spin. Rather than and admitting that they got things wrong Labour blame others.

Kevin Marshall