Suyts quite rightly criticizes Paul Krugman on the Nobel Laureate’s latest ramblings. However, his analysis misses a couple of issues. This is an extended comment.

You are quite right on two issues here, which I believe have been called the ratchet effect and the debt servicing impact.

The first is that it is easy to increase government expenditure, but much more difficult to scale it back as there are entrenched interests to stop the scale back. It is easy to give people welfare benefits or create jobs. But try to take these away and people will fight like crazy to keep them.

The second on debt servicing you demonstrate very well. As total debt goes up, so does the interest on that debt.

There are other issues that should be taken into consideration on the deficit and debt problem.

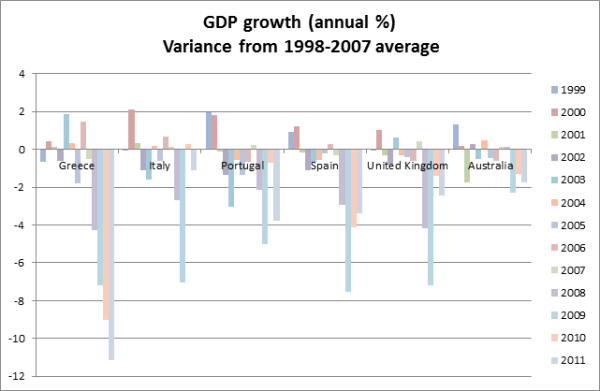

The first issue is the size of government. When an economy enters recession, the tax receipts fall and expenditure rises. Corporation tax is the first area to go down, followed by income tax as unemployment rises. In expenditure terms, welfare payments will rise along with (possibly) business bail outs. With small government, taxing little and spending little, this impact was small. With large government – in Britain rising nearly 50% of GDP – this effect is large. A 6% decline in GDP perhaps increased the deficit by 6-7% of GDP. Under the Eisenhower administration, a similar decline would worsen government finances by maybe 2% of GDP. Big government exacerbates the size of cyclical swings.

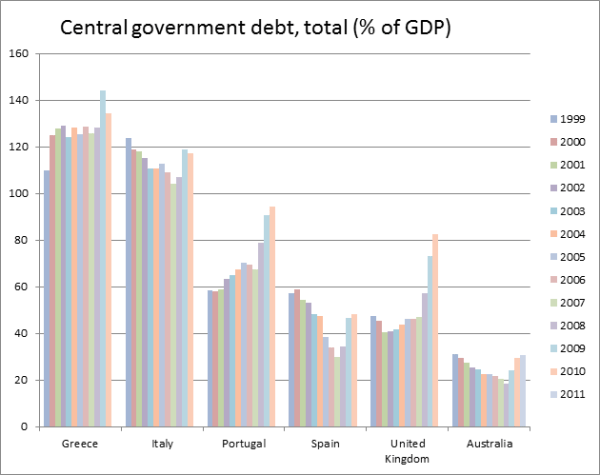

The second issue is the position at the start of downturn. In mid-2008 both USA and Britain had structural deficits – in the USA to finance the wars in Iraq and Afghanistan, in Britain finance a huge increase in public sector pay and capital spending on schools and hospitals. A structural deficit is the measure of the average government deficit over the course of the business cycle. In Britain at the top of the cycle, the actual deficit was around 3% of GDP, with a planned rise to 4%. The structural deficit was probably greater than 4% of GDP in mid-2008 in Britain and maybe slightly smaller in the USA. Below is my estimate of the impact of Britain’s structural deficit in April 2010. I estimated that the structural deficit built up between 2001 and 2008 would in the long-term increase National Debt by 40% of GDP. I was overly optimistic in my assessment.

The third issue is with the classical Keynesian Multiplier. Crude textbook Keynesianism of the 1960s for a closed economy stated

E = C+I+G

Or national expenditure is the sum of Consumption, Investment and Government expenditure.

The theoretical impact of increasing government expenditure on total output, when the economy is at less than full employment, is Y/G. If government expenditure is 10% of national income, then increase G by $1 and Y will increase by $10. If government expenditure is 40% of national income, then increase G by $1 and Y will increase by $2.50. However, crudely put, if the government expenditure does not take up the slack in the economy (the deficit in aggregate demand), then (in an inflation-free economy) the government expenditure “crowds out” private expenditure. Another way of putting the situation, if the economy is not “stuck in a rut” as Keynes assumed in his “General Theory”, but merely reacting to overinvestment (such as a housing bubble), then increased government expenditure will have no effect on total output, but “crowd out” other expenditure. It will also add to the nominal national debt, without adding to total national income, thereby increasing national debt as a percentage of national income, or expanding national income leading to increased tax revenues and thus closing the deficit.

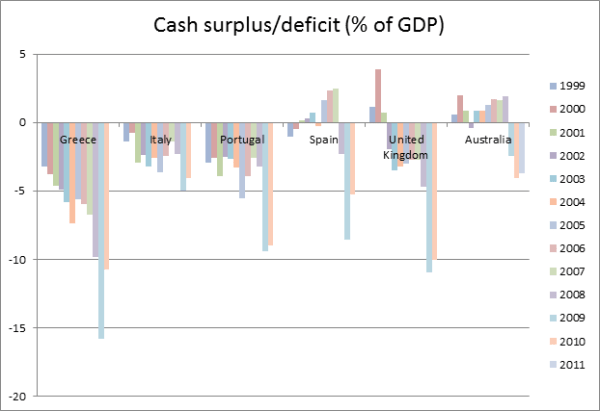

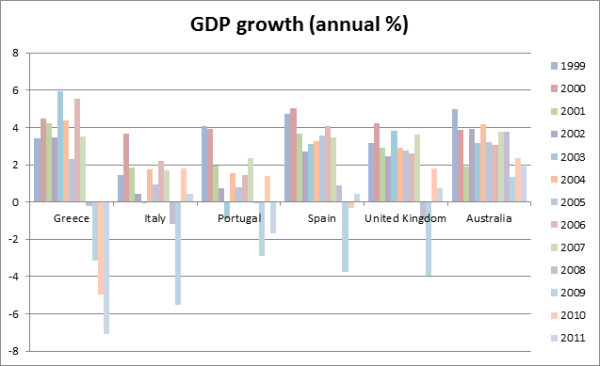

The fourth issue is fiscal tipping points. If the increased government expenditure fails to stimulate the economy, then the result will be a larger structural deficit. If, like some European countries, there is a further contraction then the deficit will increase. In Greece, Spain, Italy and Portugal, this further downturn has led to increased economic risk, pushing up interest rates. This increases short-term debt costs, further increasing the deficit. The only way to stem total collapse is to massively cut public expenditure and increase taxes to not only pay for the debt-financing costs but to rapidly cut the deficit as well. In climate change there has been much spurious talk about possible tipping points in the remote future if certain things come true. But in OECD economies, with some already having gone beyond the fiscal tipping points, many (including Krugman) seem oblivious to the possibility. Should we not use a smidgeon of the precautionary principle in economics , proclaiming austerity as an insurance against severe depression.?

Kevin Marshall